Customer Loyalty Blockchain: Ecommerce Shops Take Advantage of Blockchain Rewards Programs

Customer Loyalty Blockchain: Ecommerce Shops Take Advantage of Blockchain Rewards Programs

Get The Print Version

Tired of scrolling? Download a PDF version for easier offline reading and sharing with coworkers.

A link to download the PDF will arrive in your inbox shortly.

Retailers and ecommerce sellers can’t underestimate the value of a loyal customer. With customer acquisition costs rising and new competitors always waiting in the wings, building a strong cadre of customers who value your brand above all others and are willing to spread that message to their friends is a huge advantage.

Here are just a few stats on the value of loyal customers.

Repeat customers generate 40% of a store’s revenue.

62% of millennial shoppers and 54% of the larger population tend to only buy from their preferred brand.

The top 10% of customers spend 3 times more per order than the average customer. The top 1% of customers spend 5 times more.

Overall, loyal customers spend more, are more likely to convert when they visit your site, and are more likely to become brand promoters and champion your brand to other potential customers.

Since loyal customers are such a hot commodity, it’s no wonder that brands are spending more to court them. Of Fortune 500 companies surveyed, 54% said they would be increasing their loyalty program budgets in the 2017-2018 fiscal year.

For a long time, ecommerce and brick-and-mortar stores have used loyalty programs to encourage repeat business. Traditionally these programs have been used as a tactic to encourage repeat customers by offering points and discounts.

Sometimes involving cards or complex registration processes, these programs are beginning to fall out of favor with modern customers. Instead of heightening the customer experience, they can actually have the opposite effect — dampening customer enthusiasm with complex rules and transactional rewards.

One solution that some businesses are coming to embrace is implementing blockchain technology for customer loyalty. The hope is that blockchain technology will revolutionize customer loyalty rewards by eliminating some of the pain points of traditional programs.

What is Blockchain?

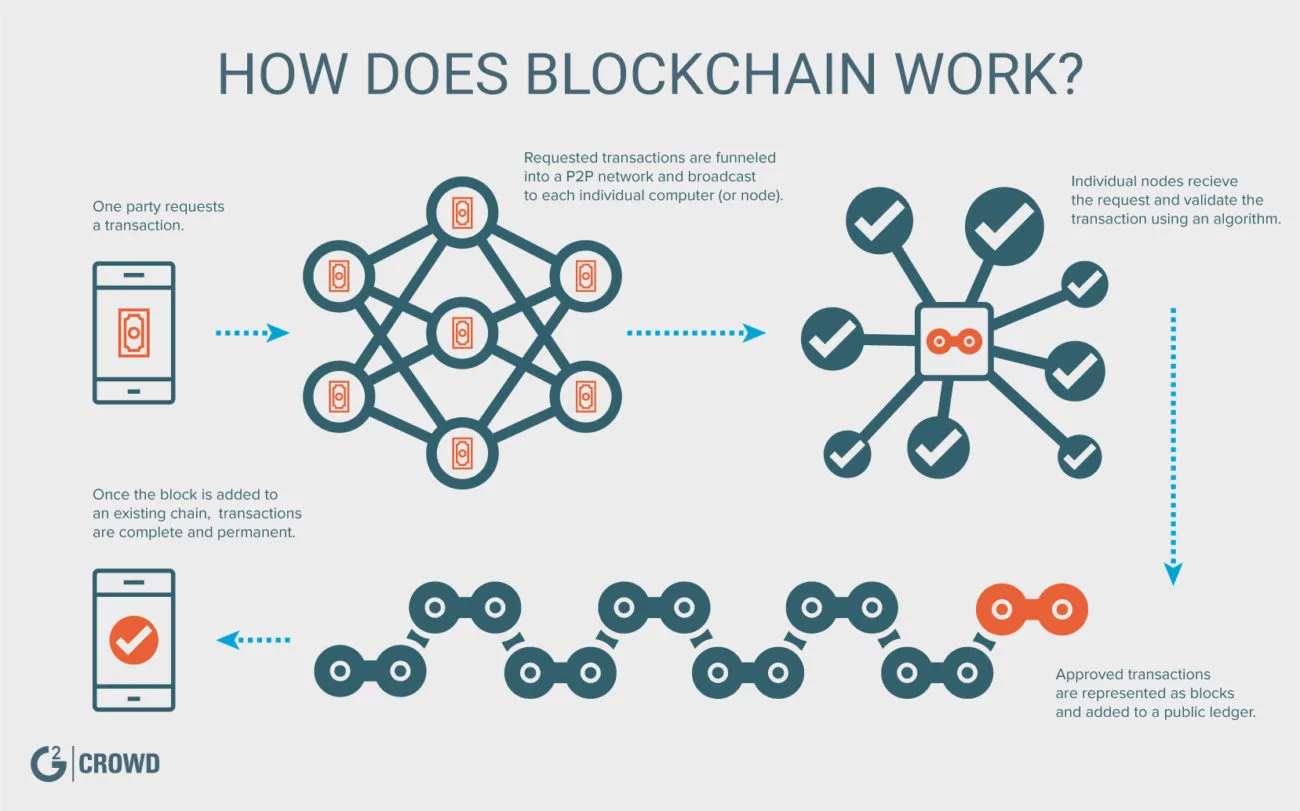

Blockchain is a decentralized method of taking transactions and accounting for them. The “blocks” here are storage units for digital information about transactions — like the date, time, amount, and parties participating in the transactions. Each block includes a unique code called a hash that allows it to be distinguished from every other block.

When new transactions are made, new blocks are added to the end of a chain, which is a public database available for anyone to view. Blockchain technology is broadcast off of a P2P system of nodes, makes it more anonymous and secure than other forms of payment. Because each block contains a unique hash, hackers can’t easily tamper with the data.

Image from: https://www.g2.com/categories/blockchain

Blockchain technology as a concept has been around since the early 1990s, but it gained traction in 2009 as it became the ledger that backed transactions associated with the cryptocurrency Bitcoin.

Blockchain is a natural fit for ecommerce because it is designed for storing transactional data in a way that is secure and decentralized.

Now that you have a rundown of what blockchain technology is, let’s deep dive into why blockchain technology is a good fit for revamping customer loyalty programs.

Customer Loyalty Programs Need an Upgrade

In ecommerce, it is usually quick and easy for a consumer to sign up for a retailer’s loyalty program. But how many of your customers are actually becoming a loyal advocate to the brand?

Traditional loyalty programs suffer from the following issues.

1. Low redemption rates.

Perhaps because of the large number of loyalty programs in the market, it’s easy for them to get lost in the shuffle, and points go unredeemed. Surveys show that the average American is a member of 7 loyalty programs, and 30% of American consumers never redeem a single point. Until those points expire (if they ever do), they just sit there as a liability on a brand’s bottom line, having failed at earning repeat business.

2. High costs.

Large stores and successful ecommerce shops often pay high prices to setup and maintain their third-party integrations or custom solutions for customer loyalty programs. Whether they are making adjustments to an existing app or building their own from scratch, developer and maintenance fees can range from $2K – $15K a month for an enterprise-level solution. Understandably, if you are not seeing a strong ROI from reward program costs, it’s not worth it to keep the program.

3. Few customer incentives.

Today’s loyalty programs tend to favor the company providing them, instead of the consumer. For example, customers are forced to make purchases they don’t need in order to reap the rewards.

Research also indicates that 33% of millennial consumers dislike reward programs simply because there are too many cards to carry. If your loyalty program isn’t fostering a positive relationship with your consumers, what’s the point of it?

4. Security concerns.

Some consumers may be wary of data breaches and the security of the information they give out when joining a loyalty program. A Harris Poll found that 71% of consumers were less likely to join a loyalty program that collected personal information beyond just name and phone number. They are right to have some concerns. In 2017, 11% of attacks on financial accounts were specifically on loyalty accounts, an amount that had risen from 4% the year before.

6 Cases for Blockchain Loyalty Tokens

Blockchain technology can solve for some of these issues with traditional ecommerce loyalty programs by connecting owners and users of multiple programs.

This technology can simplify the process of applying and keep consumers from having wallets overflowing with rewards cards or passwords to multiple different reward accounts.

Through blockchain, users can receive and redeem loyalty tokens that are interoperable across multiple programs.

These tokens never expire or lose value, unlike traditional reward points. Here are a few of the advantages to this type of system.

1. Open systems.

Owning a blockchain token cannot be revoked and is recorded publicly on the blockchain. The issuing company cannot take away those points due to some internal policy. This is both a win for the consumer who doesn’t have to worry about their points expiring or being devalued before they can use them, and a win for businesses who gain greater customer loyalty by providing a better and more transparent customer experience.

2. Less clutter.

Blockchain tokens can be used at other stores, switched for different cryptocurrency, or stored for a future time. That means consumers won’t have to juggle 600 Vons points, 50,000 American Airlines miles, and 10 sandwich card stamps.

3. More flexibility.

With blockchain loyalty tokens, customers have more freedom in how they redeem their tokens, including being able to redeem them in smaller increments. One of the complaints many customers have with loyalty programs is the complex point accrual systems and limited rewards, so allowing for more flexibility in how they use the rewards they’ve earned is a huge plus.

4. Reduced costs.

Program costs won’t take years and hundreds of thousands of dollars to implement and maintain. Because of Blockchain’s native ledger, you already have a loyalty record.

5. Overall transparency.

Users will know that companies cannot change rules or blockchain token amounts based on their will. This gives customers satisfaction that they can redeem what they want, when they want.

6. Less fraud, more security.

Blockchain is based on P2P systems, meaning there is a far less likely chance of a breach in the program or in your store in general. All necessary information is stored on the immutable blockchain ledger. The time-stamped database entries are irreversible preventing issues of fraud and transaction manipulation.

4 Reasons Ecommerce Needs Blockchain

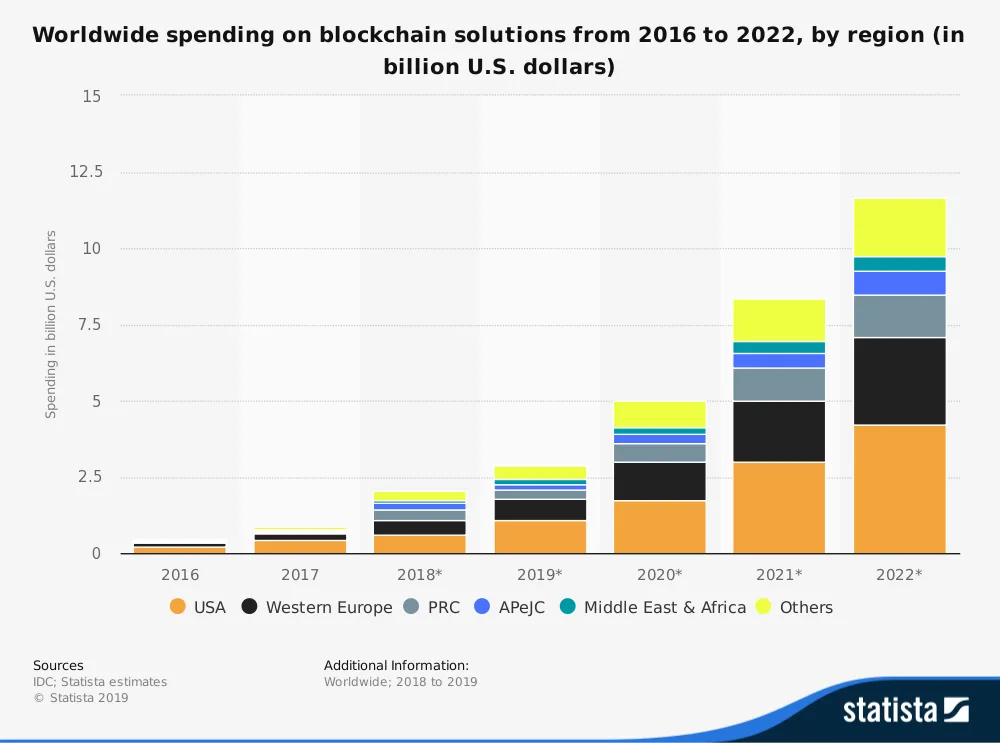

Blockchain is expected to surge in the coming years due to its value-add for businesses. A Gartner forecast posits that the value of blockchain for businesses will exceed $3.1 trillion by 2030.

Businesses are responding to this potential value in kind by investing in new solutions. This graph shows the global spending on blockchain solutions in recent years and projected through 2022.

What exactly is behind this value-add and how will blockchain disrupt ecommerce?

1. Easier implementation for shops of all sizes.

One of the reasons blockchain can be a game changer for ecommerce and retail businesses is that it opens doors for smaller businesses to create loyalty programs of their own. Because the loyalty program can be implemented at a lower cost, it can be achieved on a smaller scale with less barrier to entry for new and small businesses.

2. Better accounting.

In addition to reduced costs, another advantage is streamlined account management. Blockchain isn’t just simpler for customers to manage without having to juggle multiple cards and accounts. From the business side, you won’t need an accounting team to have spreadsheets worth of numbers on who spent what and whose points are where.

3. Happier customers.

Ecommerce is competitive, and businesses know they need strategies beyond just having a compelling product to not only attract customers, but keep them coming back. Giving customers rewards for being loyal is one way to achieve return customers to an online store. With blockchain, ecommerce stores can revamp their loyalty programs to make customers happier because they will have a greater ownership and flexibility over their rewards and a more frictionless overall experience.

4. Access to a network of loyal customers.

By using blockchain to create a network of partnerships where consumers can use their tokens, a business gains access to an ecosystem of potential customers.

Businesses Adopting Blockchain Loyalty

Currently, blockchain rewards programs are still not exactly mainstream. However, there are a few businesses paving the way and exploring the potential of the technology. Here are a few examples.

1. Singapore Airlines.

In July of 2018, Singapore Airlines announced that their frequent flyer program KrisFlyer would now be reinvented as KrisPay, a miles-based digital wallet which members could use to convert miles into digital spending power with other merchants.

At launch, KrisPay was partnered with 18 merchants through categories ranging from beauty and food services to gas and retail. The press release announcing KrisPay describes it as “the world’s first blockchain-based airline loyalty digital wallet.”

2. Chanticleer Holdings.

Another pioneer in the world of blockchain rewards is Chanticleer Holdings an investor in several chain burger restaurants including BGR, Little Big Burger, and American Burger Co. In January 2018, they announced a collaboration with MobivityMind, a blockchain architecture platform.

As part of their new loyalty program, customers who eat at one of their restaurants now receive a type of cryptocurrency called Mobivity Merit which can be redeemed across brands and traded with no fraud concerns.

As Chanticleer Holdings CEO Michael D. Pruitt explains: “We’re excited to see how consumers respond to the idea of getting real, transferable, secure value in exchange for their loyalty to our brands.”

3. American Express and Boxed.

No stranger to rewards and loyalty programs, in May of 2019 American Express announced a blockchain test program with online wholesale retailer Boxed. Using a blockchain framework, AmEx created a private system for Boxed to transfer information which merchants on Boxed can use to fulfill rewards program offers.

Essentially, when a consumer makes a purchase on Boxed, the blockchain stores the data about the transaction (while hiding privileged data about the card holder). The details of the transaction trigger the creation of a smart contract which then creates and awards points in a backend loyalty system.

Conclusion

The ecommerce industry is always changing along with customer expectations. Customer pain points today will inform the innovations of the future.

Blockchain technology for loyalty programs is still somewhat in its infancy, but may cause greater disruption in the industry as more brands explore the capabilities.

It wil be illuminating to see how this emerging technology scales as more and larger companies consider transitioning their traditional loyalty programs or building new ones through blockchain.

Chris Shalchi is an established eCommerce leader in providing growth and cost-saving strategies for Fortune 500 companies. Chris often appears on eCommerce technology strategy panels for BWG Strategy and eCommerce Advisory and technology podcasts eCommerce Q&A and Commerce Hero. He has lead global eCommerce solutions for organizations like Volvo-Eicher Ferrari and Guggenheim Partners. Chris is a Senior Executive for BigCommerce; CPG merchant, keynote speaker, father and songwriter.